In English below

Um artigo importante de Marcello Minenna publicado no blog FT Alphaville examina a partilha de risco entre os países credores (do centro) e devedores (da periferia ou da suposta "convergência") ao longo da crise da Eurozone de 2008-2018 para determinar quem efectivamente beneficiou mais com os resgates da Troika, do ECB e das instituições europeias.

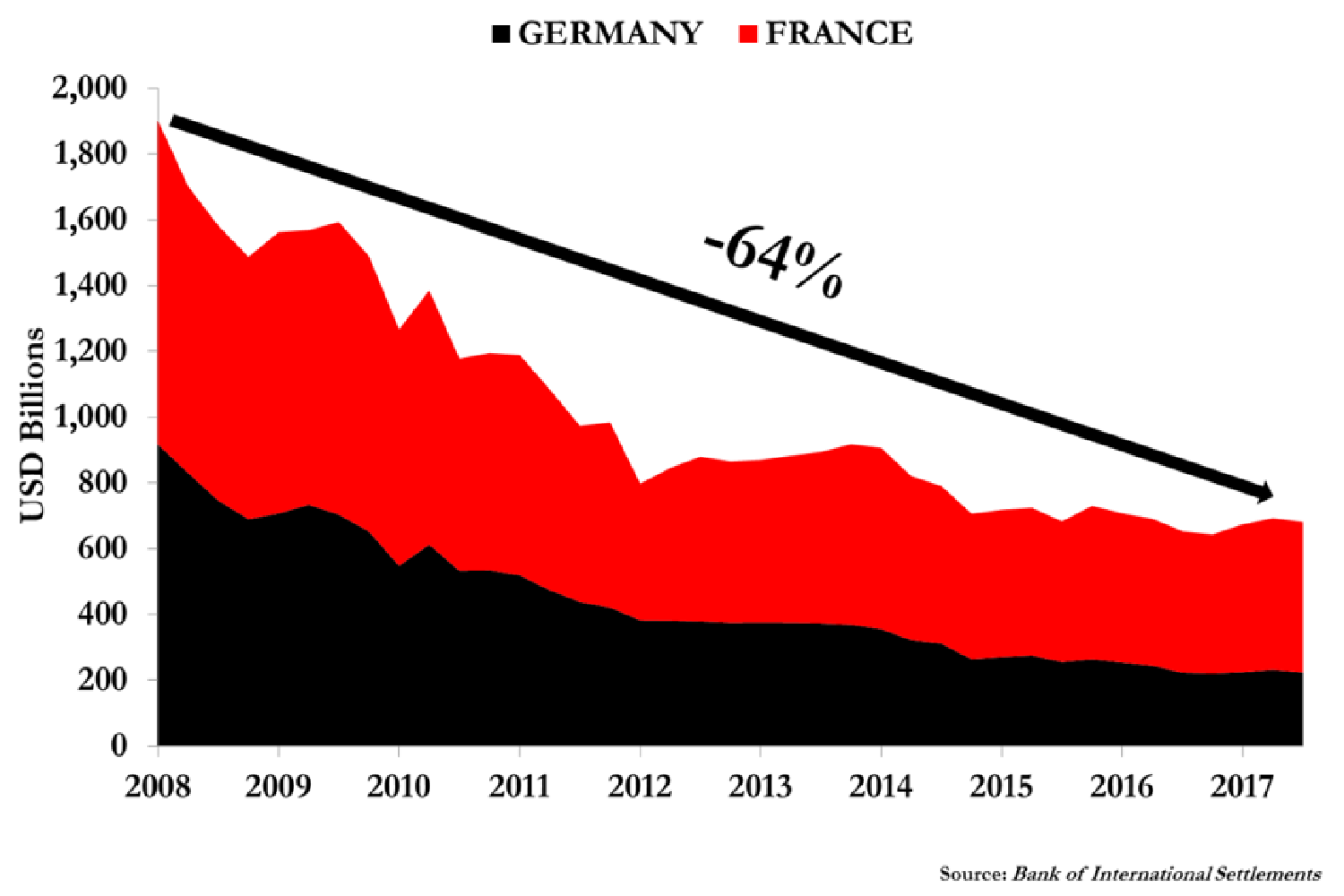

Com base nos dados do o Bank for International Settlements (BIS), a exposição total das instituições financeiras francesas e alemãs aos países mais endividados da periferia foi rapidamente reduzida de 2010 até 2012 graças à substituição de credores comerciais (bancos e investidores privados) por credores oficiais (ECB/BCE, EU, FMI)

Esta substituição de credores, muito visível no caso da Irlanda, evitou que o Bundesbank e o Banco de França tivessem que apoiar tanto os seus bancos imprudentes.

Esta substituição de credores, muito visível no caso da Irlanda, evitou que o Bundesbank e o Banco de França tivessem que apoiar tanto os seus bancos imprudentes.

Diz o artigo:

"A narrativa comum é que os programas de resgate ajudaram países profundamente problemáticos a evitar a falência soberana ou as falências bancárias generalizadas. Mas, ao evitar resultados extremos, esses programas também protegeram os bancos dos países centrais - Alemanha e França, em particular - que tinham acumulado enormes exposições aos países da periferia antes da crise. À época, esta partilha de riscos (embora desagradável) era a melhor opção disponível para os governos dos países centrais. Isso salvou-os de ter que intervir (à custa de seus próprios contribuintes) para sustentar seus próprios sistemas bancários nacionais."

O aumento de exposição dos credores espanhóis desde 2014 está a tornar Portugal numa colónia financeira de Espanha, diz o FT Alphaville

Digo eu:

Também podíamos afirmar que o novo endividamento externo de Portugal está a criar uma bolha à vista desarmada que há-de rebentar mais cedo e não mais tarde.

Mariana Abrantes de Sousa

Economista

"According to the Bank for International Settlements (BIS), in 2010 the total exposure of French and German financial institutions to the pheriphery countries.

The common narrative is that rescue programs have helped deeply troubled countries avoid sovereign bankruptcy or widespread bank failures. But, by avoiding extreme outcomes, these programs also protected the banks of the core countries — Germany and France, in particular — that had accumulated huge exposures to the periphery before the crisis. At the time, risk sharing (however unpleasant) was the best available option for the governments of the core countries. It saved them from intervening (at the expense of their taxpayers) to prop up their own national banking systems.

The size of all of this deleveraging can be measured by using BIS data on the consolidated position of foreign banks to counterparties residing in Italy, Greece, Spain, Portugal and Ireland.

After having accumulated a whopping credit towards the periphery in the period 2000-2008, these banks have dismantled 64 per cent of their exposures in the following decade. Indeed, at its peak (June 2008) the total exposure of the Franco-German banking system to the periphery exceeded $1.9trn; in June 2012 it had already fallen to $800bn and in the following five years, it decreased further, reaching $680bn at the end of 2017.

In terms of direct exposures, on the eve of the crisis, Germany was leading in Spain ($315.5bn), Ireland ($240.7bn) and Portugal ($52bn), while France in Italy ($553.4bn) and Greece ($86.1bn). But in reality, a good chunk of French investment in Southern Europe was channeling German savings. This was followed by a colossal disinvestment from the periphery countries– over $1.2 trn"

Ver artigos anteriores sobre a problemática da GED-Gross External Debt, Divida Externa Bruta e a Crise https://ppplusofonia.blogspot.com/2012/06/us-and-uk-banks-increased-potential.html

Um artigo importante de Marcello Minenna publicado no blog FT Alphaville examina a partilha de risco entre os países credores (do centro) e devedores (da periferia ou da suposta "convergência") ao longo da crise da Eurozone de 2008-2018 para determinar quem efectivamente beneficiou mais com os resgates da Troika, do ECB e das instituições europeias.

Com base nos dados do o Bank for International Settlements (BIS), a exposição total das instituições financeiras francesas e alemãs aos países mais endividados da periferia foi rapidamente reduzida de 2010 até 2012 graças à substituição de credores comerciais (bancos e investidores privados) por credores oficiais (ECB/BCE, EU, FMI)

Diz o artigo:

"A narrativa comum é que os programas de resgate ajudaram países profundamente problemáticos a evitar a falência soberana ou as falências bancárias generalizadas. Mas, ao evitar resultados extremos, esses programas também protegeram os bancos dos países centrais - Alemanha e França, em particular - que tinham acumulado enormes exposições aos países da periferia antes da crise. À época, esta partilha de riscos (embora desagradável) era a melhor opção disponível para os governos dos países centrais. Isso salvou-os de ter que intervir (à custa de seus próprios contribuintes) para sustentar seus próprios sistemas bancários nacionais."

O aumento de exposição dos credores espanhóis desde 2014 está a tornar Portugal numa colónia financeira de Espanha, diz o FT Alphaville

Digo eu:

Também podíamos afirmar que o novo endividamento externo de Portugal está a criar uma bolha à vista desarmada que há-de rebentar mais cedo e não mais tarde.

Mariana Abrantes de Sousa

Economista

"According to the Bank for International Settlements (BIS), in 2010 the total exposure of French and German financial institutions to the pheriphery countries.

The common narrative is that rescue programs have helped deeply troubled countries avoid sovereign bankruptcy or widespread bank failures. But, by avoiding extreme outcomes, these programs also protected the banks of the core countries — Germany and France, in particular — that had accumulated huge exposures to the periphery before the crisis. At the time, risk sharing (however unpleasant) was the best available option for the governments of the core countries. It saved them from intervening (at the expense of their taxpayers) to prop up their own national banking systems.

The size of all of this deleveraging can be measured by using BIS data on the consolidated position of foreign banks to counterparties residing in Italy, Greece, Spain, Portugal and Ireland.

After having accumulated a whopping credit towards the periphery in the period 2000-2008, these banks have dismantled 64 per cent of their exposures in the following decade. Indeed, at its peak (June 2008) the total exposure of the Franco-German banking system to the periphery exceeded $1.9trn; in June 2012 it had already fallen to $800bn and in the following five years, it decreased further, reaching $680bn at the end of 2017.

In terms of direct exposures, on the eve of the crisis, Germany was leading in Spain ($315.5bn), Ireland ($240.7bn) and Portugal ($52bn), while France in Italy ($553.4bn) and Greece ($86.1bn). But in reality, a good chunk of French investment in Southern Europe was channeling German savings. This was followed by a colossal disinvestment from the periphery countries– over $1.2 trn"

So much for convergence !

Ler mais em https://ftalphaville.ft.com/2018/10/10/1539147600000/A-look-back--what-Eurozone--risk-sharing--actually-meant/ Ver artigos anteriores sobre a problemática da GED-Gross External Debt, Divida Externa Bruta e a Crise https://ppplusofonia.blogspot.com/2012/06/us-and-uk-banks-increased-potential.html